Cash In Lieu of Repairs

Cash in lieu of repairs is an option the insurance company and yourself have to finalise a claim. The insurance companies liability lies at the repair cost as to what it would have cost them had they repaired your vehicle.

If you are going to complain about the insurer’s offer of settlement, i would suggest you DO NOT ask for a CIL, as this ‘may’ give the opportunity to an insurer to try and offer less,but force them to give it to you.Ie elect to use your own repairer.

What is a cash in lieu settlement? And what are my entitlements? Insurance companies can settle a claim by one of three different ways.

Repair your car.

Total loss your car.

Provide Cash settlement.

Insurers call giving you the cash, to provide “cash in lieu of repair” (CIL) ie..rather than repair your car, they provide you with the funds to do so.

An insurer can “opt” to provide a cash in lieu settlement(CIL) for a number of reasons. An insurer may find that your vehicle has been repaired poorly in the past, or it has corrosion in the same area of damage.

When an insurer repairs or arranges the repair of your vehicle, they are ‘Corporately liable’ for any injuries that you or other people may sustain as a result of any defective works carried out that they have authorised. An insurer is only ever liable for the cost of repair, technically they should not be arranging them at all.

An insurer is not liable for the poor previous repairs or corrosion that may be there on your vehicle. They would argue that “betterment” ( you are being put in a better position as a result of the accident than the contract allows) would occur should they repair your vehicle, due to this they may elect to provide “Cash In Lieu of Repair” to fulfil the contract they have.

Insurer’s may also advise they will provide a CIL when the parts required to repair your vehicle are no longer available.

Should you wish to arrange your own repairs, you may find the insurer becomes very awkward and will advise they will pay YOU a CIL rather than authorise repairs at your choice of repairer.

They may also suggest they will only pay what it would cost them to repair at their approved repairer.

You have the lawful entitlement to have your car repaired where you wish, and the contract of insurance is there to indemnify you for your loss, ie you should be no better or worse off as a result of the incident. Your insurer may well be in breach of contract if they do not cover the full cost of repair that you have incurred in having your vehicle repaired at your choice of repairer.

An “Offer” of “Indemnity” is not “providing indemnity” if the contract has not been fulfilled.

A common excuse insurer’s come up with is ” we will not pay the vat on the estimated cost of repair” and in doing so offer you 20% less than you are entitled too.

This is COMPLETELY WRONG!, Any insurance claim is a “compensatory amount” and is not subject to VAT, the fact they use repairers that are vat registered is not your fault. Whether it cost £1000 to repair your vehicle at repairer a repairer who is not vat registered, or £1000 at one who is makes NO difference to you as the consumer.

Can I request for a Cash In Lieu of Repair?

Yes you can, and it can be a good way to avoid your vehicle from being a total loss. This particularly applies to older vehicles.

It may well be if you discuss with the insurer that you can agree a CIL at less than the market value and you repair the vehicles using non original or Green parts to save it from being a total loss.

This saves your vehicle from having a total loss category applied, keeps your insurance policy running, is better for the insurer as they retain your custom, and keeps you happy.

It also means the insurer holds no liability for the repairs carried out. From an insurer’s viewpoint all positive.

Your insurance company may “offer” you a lower figure than it cost to repair your vehicle.They are not allowed to do this, and they are not playing fair.The above is a complaint that went to the Financial Ombudsman ,and that was their ruling.

They advise the insurer should pay the full repair cost INCLUDING VAT. Often insurance companies may advise they will pay less the VAT as they do not have an invoice to claim the VAT back.

This is completely incorrect, as insurers CANNOT claim the VAT element back.

Insurance companies are NOT VAT registered.

http://www.hmrc.gov.uk/manuals/vitmanual/vit13500.htm

VIT13500 – VAT Input Tax basics: insurance claims Insurers cannot recover any VAT incurred in obtaining replacement goods or having repairs carried out for a policy holder. The supply of goods (or services in the case of repairs) is considered to be made to the policy holder. This is so even when payment is made directly to the supplier by the insurer.

Subject to the normal rules a VAT registered policy holder may treat any VAT incurred on the supply as input tax. The insurer will normally pay the policy holder compensation exclusive of VAT. The policy holder will pay the supplier the tax and recover it as input tax.

If an insurance claim is for loss or damage at a domestic property you should make sure that any VAT claimed as input tax relates only to goods used for a business purpose.

For VAT purposes payments received by policy holders from insurers are treated as compensation for the loss incurred. They are not consideration for any supply made by the policy holder.

In the case of repairs to motor vehicles all the VAT incurred may be claimed as input tax even if there is mixed business and private use of the vehicle.

Most insurance claim forms ask the policy holder if they are registered for VAT. The insurer will either make a tax inclusive or tax exclusive payment to the policy holder depending upon the answer.

However, answering yes to this question does not establish entitlement to recover input tax on the lost or damaged goods. The policy holder and insurer should resolve the matter between themselves if the policy holder is not entitled to make full recovery of input tax. This could be due to non-business use or because the taxpayer is partly exempt. HMRC staff will not negotiate on behalf of either party.

Some policies provide insurance against the cost of legal services which may be required in connection with an insurance or indemnity claim. As with other supplies of goods or services, where payment is made by the insurer the provision of legal services is regarded as being made to the policy holder. Input tax may be deducted by the policy holder in cases where the legal services are used for the purpose of the business.

This is not your problem, its theirs….feel free to copy the above and send to any insurer that is being awkward with you as THIS IS what your entitled too.This is direct from the Financial Ombudsman who decide whether your being treated fairly or not.

I regularily read the FOS website for adjuducator decisions in a complaint case’s on DRN1593512 they have again advised that the insurer has to pay the vat click here to go to the case of the fos website.

Ref: DRN15935123

– pay Mr G £196.95 to represent the difference between the amount of £513.74

already paid to him, and the revised cash-in-lieu offer of £710.69;

– pay Mr G £142.14 to cover the cost of VAT on the work covered by the cash-in-lieu

settlement;

– pay Mr G £100 in addition to the £100 already paid, for his inconvenience through

this matter.

Cathy Bovan

ombudsman”

Notice

VAT Notice 701/36: insurancePublished 12 February 2013

Contents

- Foreword

- 1. Introduction

- 2. VAT and insurance transactions

- 3. VAT and particular supplies of insurance

- 4. Insurance supplied with other goods or services

- 5. Insurance claims

- 6. Insurance supplied outside the UK

- 7. Accounting for VAT on insurance transactions

- 8. What are insurance related services

- 9. Insurance brokers and agents

- 10. VAT and particular supplies of related services

- 11. Related services supplied with other goods or services

- 12. Insurance related services supplied outside the UK

- 13. Accounting for VAT on insurance related services

- Your rights and obligations

- Do you have any comments or suggestions?

- Putting things right

- How we use your information

5.5 Financial indemnificationIf an insurer settles an insurance claim by paying money by way of financial indemnification to the insured party, no supply has taken place for the purposes of VAT. The money paid by the insurer in settlement of the claim is therefore outside the scope of VAT.

*******New update as of the 15.08.2016 in relation to VAT and insurer’s click here to go to the Government website https://www.gov.uk/government/publications/vat-use-and-enjoyment-of-insurance-repair-services/vat-use-and-enjoyment-of-insurance-repair-services

******new update 28.09.2016 in relation to VAT, click HERE to go to the governments website. https://www.gov.uk/government/publications/revenue-and-customs-brief-15-2016-vat-use-and-enjoyment-of-insurance-repair-services/revenue-and-customs-brief-15-2016-vat-use-and-enjoyment-of-insurance-repair-services

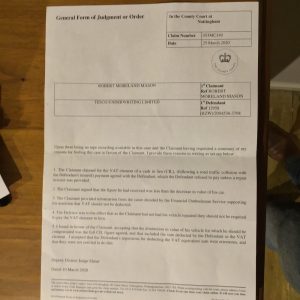

Another edit!!!! 11.05.2020

Motorclaimguru takes Tesco insurance to Court and wins!!!! https://www.motorclaimguru.co.uk/blog/can-you-claim-the-vat-element-of-repair-on-a-cil-cash-in-lieu-yes-the-courts-find-in-favour-of-motorclaimguru-v-tesco-insurance?preview_id=11580&fbclid=IwAR2UFRiDz65S49L21OVLmpM4Ul9qHzxhY4HbrHVE0N2J4FVj08mHMj-VQt4