Damaged Toyota Alphard

Imagine that you are sitting at home, your recently purchased piece of pride and joy parked outside, and you here a mighty crash. What the absolute “F#%£%} was that???????????

Then also imagine looking out of your window, to see the freshly imported car that you spent six months looking for as above. On looking down the street, you can see complete carnage, as a car has run through a junction, been T boned, and virtually sent into orbit. As a result , that car has then hit your car amongst others. Soul destroying,

However , you look at the vehicle, and you are fairly confident it can be repaired. After having spent so much time locating the vehicle, and waiting for it to be imported, it was absolutely vital in your eyes that the car was repaired. This being a “Non Fault incident” it is imperative to know your lawful entitlement.

Your lawful entitlement is here https://www.motorclaimguru.co.uk/what-are-my-rights-on-a-non-fault-claim

You contacted your insurer “Admiral” who without even seeing the vehicle declared it a total loss. ( This happens a lot, and winds me up no end! Ed). You advise that you want it repairing ( which you are fully entitled to the cost of repair up to the market value), and they ignored you.

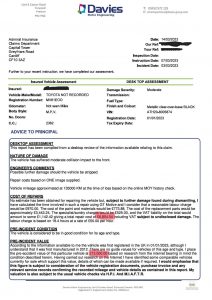

They then arranged for the vehicle to be assessed by way of images through WD Davies Group, who calculated the cost of repair at £6854.54 with a proviso of “may be subject to stripping. They then valued the vehicle at £12,000. They did this by valuing the completely wrong vehicle,. However, bearing this in mind, with a repair cost at £6854.54, and a value at £12k, the vehicle is repairable!!!!.

The customer also advised that he had recently purchased the vehicle for £19,999 less than three months previously.

But Admiral ignored this fact, and the customer’s lawful entitlement to the TORT they had been subjected too, and the legal duties under the “Financial Services and Markets Act2000 ” to comply with the FCA regulations.

I often draw to the attention the regulations too insurers in my communications, the specific two I drew to Admiral was the “Customers Best interest Rule” ICOB 2.5-1, and ICOBS 8.3.3 “Conflicts of interest”.

https://www.handbook.fca.org.uk/handbook/ICOBS/8/?view=chapter

Conflicts of interest

- (1)Principle 8 requires a firm to manage conflicts of interest fairly. SYSC 10 also requires an insurance intermediary to take all reasonable steps to identify conflicts of interest, and maintain and operate effective organisational and administrative arrangements to prevent conflicts of interest from constituting or giving rise to a material risk of damage to its clients.

- (3)If a firm acts for a customer in arranging a policy, it is likely to be the customer’s agent (and that of any other policyholders). If the firm intends to be the insurance undertaking’s agent in relation to claims, it needs to consider the risk of becoming unable to act without breaching its duty to either the insurance undertaking or the customer making the claim. It should also inform the customer of its intention.

- (4)A firm should in particular consider whether declining to act would be the most reasonable step where it is not possible to manage a conflict, for example where the firm knows both that its customer will accept a low settlement to obtain a quick payment, and that the insurance undertaking is willing to settle for a higher amount.

When you have been subjected to a TORT your insurer cannot act in conflict with your lawful entitlement. Yet it was clear in this case that they were.

This customer disputed the valuation with Admiral, advised he had paid £20k for it less than three months ago,.

There response as a “Final Response Letter” do not pass go, Go to the Financial Ombudsman Service is below.

Information about your complaint - sohara89@gmail.com - Gmail

Quite frankly, outstanding in the dismissiveness of the review. ( if it was ever indeed reviewed, as I cannot understand as in review, how you can get it that wrong).

THE CUSTOMER FINDS MOTORCLAIMGURU!

In outlining the situation, I advised of what the customer was entitled too in law, and also the limitations due to the Admiral issuing a FINAL RESPONSE LETTER and advising that redress should be sought at the FOS.

The customer instructed two of my services, my investigatory services to review whether Admiral had complied with the contract in place and it’s statutory requirements under the FSMA2000, and to have the vehicle valued by a highly qualified and experienced “Expert Witness” whose report is complaint with CPR35 in court.

I contacted Admiral on behalf of the customer , whilst a colleague valued the vehicle.

There are a lot of great people working at Admiral, a lot of these are in management roles, and they both care about customers and Admiral. Regretfully, a commercially driven business can often forget who its customers are, and cannot remove the blinkers of process’s, apply thought and rationality, or apply objectivity. For those who assisted and assist with all the cases I deal with ( MANY), i very much appreciate your help and empathy.

It is clear that things can be better, as this was a shit show of a case, where even on conclusion, this vehicle was not repaired.

Specialist valuation completed, and submitted, copy of sales invoice that was less than three month old, STILL!!!! Admiral did not value the vehicle at the amount paid, or in line with the report, though did increase the value from £12 thousand pounds to £17 thousand pounds. (Don’t forget that the repair cost are £6854, and are less than half the value, yet somehow they are still advising the car is a total loss). At this point the customer gives up on wanting the car repaired, as it is an EV hybrid, has now been stood for six months, and the £15k battery is probably unusable.

Admiral now Issue their SECOND final response, and to the FOS we go.

Admiral rejected the initial Adjudicator findings which found in the customers favour, today, we have the FINAL decision from the FOS>

Representative.Decision (2)

My final decision

For the reasons set out above I uphold this complaint and require Admiral Insurance

(Gibraltar) Limited to:

Settle Mr O’s claim on this basis his car’s market value at the time of the incident was

£19,999. Admiral should therefore pay Mr O the difference between this amount, and

any amount it has already paid him. Admiral is entitled to deduct any policy

excesses. 8 % interest should be paid on any amount it pays. Interest should be

calculated from the date it offered Mr O its first valuation, to the point Admiral pays

this settlement.

Pay Mr O £300 for the engineer’s report he obtained. 8% interest should be added to

this payment too. Interest should be calculated from the date Mr O paid the invoice,

to the date Admiral pays him.

Pay Mr O a total of £500 compensation for the distress and inconvenience caused

throughout this claim.

Don’t let the people who owe you money dictate how much they will give!

Always contact MOTORCLAIMGURU before you make a claim!!!! and certainly when you do.